Main Highlights

- The best cash advance and no refusal payday loans in Canada include CashMoney, iCASH, KOHO Cover, Money Mart and PAY2DAY.

- Payday loan apps provide fast application and instant approval. Loan amounts range from $100 to $1,500, while fund release can be as quick as two minutes.

- Payday loans have very high interest rates and short repayment terms. Use them only when necessary to avoid falling into a debt trap.

Payday loans can be lifesavers during emergencies, like a car or home repair. Obtaining these loans is straightforward, so you get the money fast.

We should note that payday loans via apps for instant money have high interest rates. Use them only when necessary.

In this article, we will cover the best payday loan apps, their pros and cons and how to choose what app suits your needs best.

Best Cash Advance Apps in Canada

Below is a breakdown that helps you compare the best cash advance apps with no credit check. The table below provides a glimpse into what cash advance apps offer.

| Payday Loan Lenders | CashMoney | iCASH | KOHO Cover | Money Mart | PAY2DAY |

| Loan amounts | $100 – $1,500 | $100-$1,500 | $50 overdraft protection; up to $250 | $120 to $1,500 | Up to $1,500 |

| Fund release | 15 minutes via e-Transfer | Within 2 minutes via e-Transfer | Immediately available | 15 minutes via e-Transfer | In 48 hours |

| Fees | $15-$21 per $100 borrowed | 15% of the amount borrowed | $5 a month subscription | $15-$21 per $100 borrowed | $15 for every $100 borrowed |

| Repayment period | 14 days | 1-3 installments | Anytime, as long as you pay the monthly $5 fee on time | The next pay date following the day of loan approval | 1-31 days |

| Availability | All provinces and territories of Canada | AB, BC, MB, NB, NL, NS, ON, PE, QC, SK | All provinces and territories of Canada | AB, BC, NS, ON, SK and MB | ON, BC and NS |

CashMoney

CashMoney is an online platform that gives you borrowing options when you need money fast. Since 1992, it has helped over 1 million Canadians with short-term cash needs through its app that loans you money instantly even without a job.

- How it works. Apply for a payday loan online, at a CashMoney branch or call 1-877-526-6639. To apply online, create a CashMoney account, provide the required details and submit your application. When approved, choose a loan amount, sign the contract and receive the funds.

- Requirements. A chequing account, proof of recurring source of income (unemployment and disability are accepted), working telephone number, valid identification, and an email address

- Loan amounts. $100 – $1,500 (amount varies by location)

- Approval and funding. You can get your money in cash at a CashMoney Store, via direct deposit to your bank account, or through Interac e-Transfer (in as little as 15 minutes)

- Fees. $14-$17 per $100 borrowed, depending on location (includes all fees and charges)

- Availability. Across Canada

- Pros. Easy application, instant lending decision, fast fund release through Interac e-Transfer, different options to get the money

- Cons. High interest rates (up to 356.00%), high costs, subject to qualification requirements, short repayment terms

- App download. App Store, Google Play

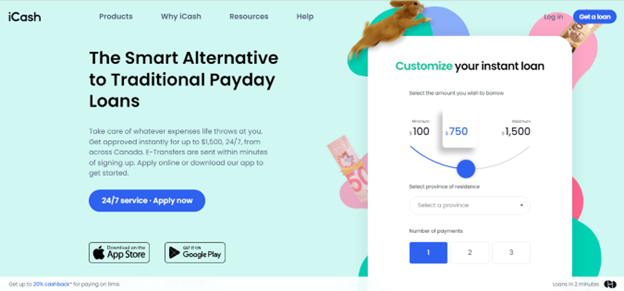

iCASH

iCash has been a provider of no-refusal payday loans in Canada since 2016. With over 850,000 members, it offers payday loans that are available in minutes and allows borrowers to earn cashback.

- How it works. Apply online or through the iCash loan app, select your loan amount and repayment plan, provide the required personal information and submit your application. Once you are approved, you can get the money within minutes.

- Requirements. At least 18 or 19 years old, a resident of any of the provinces iCash operates in, a total net income of at least $800 per month, access to an online bank account, valid mobile phone number, address and email address

- Loan amounts. $100-$1,500

- Approval and funding. Approval is instant. This cash advance app, which requires no credit check, provides your funds through e-transfer within two minutes.

- Fees. 15% of the amount borrowed

- No. of payments: Up to 3

- Availability. AB, BC, MB, NB, NL, NS, ON, PE, QC, SK

- Pros. Fast online application, instant approval, flexible repayments, 24/7 services, 100% secure process, fund release through eTransfer is at no extra cost, does not require good credit, no hidden fees, membership perks (earn up to 20% cash back on the cost of borrowing), 93% approval rate

- Cons. High interest rates and borrowing costs, short repayment terms

- App download. Google Play, App Store

Neo Secured Mastercard

Rewards: Earn up to 15% cash back at thousands of Neo partners and never fall below 0.5% average cash back.

Welcome offer: $25 welcome bonus; Get an extra 15% cash back on your first-time purchases at participating merchants.

Interest rates: 19.99% to 24.99%

Annual fee: $0

Recommended credit score:

N/A

On Neo’s website

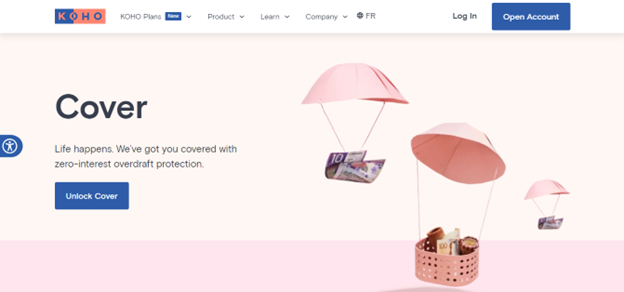

KOHO Cover

KOHO Cover from KOHO Financial is a subscription-based zero-interest overdraft protection that provides financial help during unexpected emergencies. Through this app that loans you instant money, you get coverage when you need it, while having access to a financial coach.

- How it works. Add KOHO Cover to your KOHO account and get $50 interest-free overdraft protection. When your balance is low, you will get coverage of up to $50 on any purchases. Your coverage remains for as long as you pay the subscription fee. KOHO collects the $5 fee at the end of each month.

- Requirements. You must be an existing KOHO user. To be eligible for Cover, add funds to your KOHO account, set up direct deposit, keep a balance and use your account to pay your bills.

- Loan amounts. You can get an overdraft of $50. On-time repayments may qualify you for a credit limit of up to $250. Using KOHO features like Credit Building can also help increase your Cover limit.

- Approval and funding. Upon enrolling in KOHO Cover, funds will immediately be added to your overall balance.

- Fees. $5 a month subscription

- Availability. All provinces and territories of Canada

- Pros. Interest-free overdraft limit, no application needed, no late fees, on-time repayments may increase your overdraft limits, can cancel anytime, not a payday loan

- Cons. Subscription fee of $5 per month, small loan amounts, must be an active KOHO account holder, takes time to unblock KOHO Cover access, eligibility requires a KOHO invite

- App download. App Store, Google Play

Money Mart

Money Mart is a full-service provider of payday loans with a free instant cash advance app that Canadians have used since 1982 to obtain loans. With over 500 locations across Canada, it provides services to financially underserved consumers and businesses in North America.

- How it works. Fill out the online application form and choose your preferred bank account and funding method. You can also visit a Money Mart branch to apply for a loan.

- Requirements. At least 18 years old (age varies by province), have a chequing account, be employed or have a steady income stream, most recent pay stub, a bank statement showing the last two direct deposits, a blank or voided cheque or pre-authorized debit form

- Loan amounts. $120 to $1,500

- Approval and funding. You can borrow money through this app instantly (as fast as 15 minutes via e-transfer), and within 24 hours or 1-2 days through other options.

- Fees. $15-$21 per $100 borrowed (depending on location)

- Availability. Originated only to residents of AB, BC, NS, ON, SK and MB

- Pros. Instant loan decision, quick loan approval, fast funding, transparent fees, no impact on your credit, bad credit can apply

- Cons. Very high interest rates, high-cost loans, short repayment period (next payday), not available in all provinces

- App download. App Store, Google Play

PAY2DAY

PAY2DAY is a fully licensed provider of short-term loans to Canadians needing quick cash. With over 30 locations, it offers payday loans through its cash advance app with no credit checks to eligible individuals.

- How it works. Complete the online application form and submit it. Upon approval, get the funds via e-transfer within an hour. You can also apply in-store at any of its branches or through the app.

- Requirements. Be at least 18 years old, have a bank account, have employment income (EI and retirement benefits are accepted), and have access to online banking

- Loan amounts. Up to $1,500. The maximum allowable advance is up to 50% of your net pay.

- Approval and funding. Once you complete the requirements, the fund release will be in 48 hours.

- Fees. $15 for every $100 borrowed

- Availability. ON, BC and NS

- Pros. Quick and easy application, fast approval and funding, no appraisal or legal fees, all credits can apply, no credit checks, and in-store borrowers get interest-free $300 cash advance on their first payday loan (limited time offer)

- Cons. High interest rates, not available in all provinces, and the app is not available on Google Play

- App download. App Store

What Are Payday Loan Apps?

Payday loan apps are tools used to apply for instant loans like payday loans, get instant funding and manage repayments.

Apps that loan instant money make borrowing easier and quicker by allowing you to request a small amount of money, which you repay during your next paycheck or whatever repayment option is available.

Pros and Cons of Payday Loan Apps

Payday loan apps are all about getting access to cash fast. While payday loans are beneficial in many cases, other times they may put you at risk of getting thrown into a cycle of debt. Below are the most common pros and cons of getting a payday loan via apps.

Pros

- Provide fast access to cash

- Let you borrow money through apps instantly

- Fast and easy to obtain

- Accept bad credit

- Easy eligibility

- No collateral

- Government benefits are acceptable as income

- Application, approval and fund release are typically done online

- Fast transfer of funds

Cons

- Higher interest rates and fees; APR of up to 400% (on average)

- Smaller loan amounts

- Shorter loan repayment terms

- Loan costs vary by province

- May come with late payment fees, depending on the lender

- Bounced cheques or failed direct debits if your payment bounces

- Potential to throw borrowers into credit dependency

What To Consider When Choosing A Payday Loan App

In choosing the best payday loan apps for fast money, consider the factors below to make the best choice:

- Pre-qualify. Pre-qualify for multiple payday loans to see the rates and loan terms you qualify for and to find the best deal.

- Loan cost. Compare interest rates and other fees included in the loan. Choose a lender with the lowest fees to reduce your overall borrowing cost.

- Loan terms. Review the loan terms to see if they suit your present financial status. To avoid higher interest rates, choose the shortest term. If you need to recover financially, a longer loan term may be more suitable.

- Lender reputation. Check that the lender is licensed to operate in your province or territory. Find out their reputation by checking review sites.

- Customer feedback. This is necessary to determine if a payday loan service is for you. Find testimonies that verify the quality of the services offered.

Payday Loan App Alternatives

If you are facing financial difficulty, you may first want to consider these alternatives that are less expensive than a payday loan.

Credit Card Cash Advance

If you are eligible, getting a credit card cash advance is more affordable than a payday loan. Most credit card companies allow you to borrow from your credit card limit through a cash advance. In exchange, you must pay a fee and an APR higher than when you use your credit card for regular purchases but lower than a payday loan.

Installment Loans

Apart from payday loans, installment loans provide another way to get quick access to money but with higher loan amounts, extended repayment periods (generally up to a year) and more affordable repayments. They are also cheaper than payday loans, having rates ranging from 5% to 30%.

Loans From Friends and Family

If you are strapped for cash, getting a loan from your family and friends may be better than taking out a payday loan. These loans typically come with low to zero interest and do not include late payment fees. There is also no need to worry about having a good credit score and finding cash advance apps with no credit check.

HELOC or Line of Credit

A home equity line of credit (HELOC) is a better financing option if you need extra cash. As with a payday loan, you can use a HELOC however you like, but at lower loan costs and rates. A line of credit includes an administration fee plus annual interest on the amount you borrow.

Overdraft Protection

With overdraft protection, you have a less expensive safety net than payday loans. The bank will typically cover transactions exceeding the amount in your account.

If you are short of funds, your bank will cover up to a specific amount. You will then pay what the bank covers for you plus fees and interest, which is usually cheaper than a payday loan.

Should You Use a Payday Loan App?

Free instant cash advance apps may help you obtain payday loans easily, but these loans are more expensive than other short-term loans. Due to this, you should explore cheaper alternatives before you push through with a payday loan.

You must only use a payday loan app if you can repay the loan in time and have room for other expenses. Relying too much, too often on payday loans, can pose a significant risk to your financial health and cause you to fall into a debt cycle. When possible, use other alternatives before deciding on a payday loan.

Related: